Findlay Market in Cincinnati, where a nonprofit market manager and CDC are working alongside private developers to create a mixed-use destination based around small, local shops.

Our earlier lunchtime conversation in Dallas quickly morphed into some constructive criticism of the community development field. We’re doers, so we delved into some of the mechanics of how a community could control its destiny, and ensure affordability over longer time scales.

In theory, Community Development Corporations have tremendous capacity to manage community change, but even where good CDCs exist — as in Boston and Chicago — their efforts are often quickly overwhelmed by the monstrous quantities of capital involved in gentrification. CDFIs were started to help leverage greater sums of capital, but never quite seemed to move beyond a little niche.

The work that community development organizations do is so labor-intensive that it doesn’t end up being very scalable. Some of that is good — community organizing and small-scale development in disinvested neighborhoods is tough. Some of that is bad — there’s so much bureaucracy involved in securing grants or tax-credit financing (or securing property for a Community Land Trust), and in complying with restrictions on spending that money, that staff capacity gets stretched thin.

(As a side note, why don’t we at CNU talk more often with the community development sphere? Sure, there’s some buy-in when individuals from CDCs get invited to present, but otherwise there’s scarcely any overlap. Perhaps siloization is to blame: CDCs/CDFIs have their own conferences, their own language, their own processes.)

Yet surely there are other vehicles that can provide a middle ground of financing for community development. In a gardening analogy, LIHTC-funded, CDC-built subsidized housing is like a trickle of water from a hand-carried watering can, and Wall Street money is like turning a fire hose onto your flowerbeds. Surely there’s some happy medium: a way to use local capital within a neighborhood, to fund incremental, community-positive projects that make a solid but uneventful return, over the long run.

There’s recently been a lot of renewed buzz about low-profit corporations and B-corps. Richard Plunz’s magisterial history of New York City housing shows us that many of the most innovative efforts at community-building there stemmed from just such endeavors, many underwritten by philanthropists or unions who sought investments with steady returns.

We discussed some of the innovation going on with cooperatives — the most established of low-profit, broadly-owned corporations. I talked up some experiments in the Upper Midwest, like the River West Investment Cooperative in Milwaukee, the considerable excitement around the Northeast Investment Cooperative in Minneapolis, and efforts to minimize business displacement along the Central Corridor light rail. In both cities, local capital is fostering communities of cooperative businesses in “emerging” neighborhoods. And unlike the Mondragon cooperatives, these coops are focusing on serving neighborhood needs, rather than exporting. Nationwide, a few credit unions (like Self-Help in North Carolina) have built substantial commercial-lending businesses, even in real estate.

But as much as we liked the idea of cooperatives, not everywhere has the fertile legal or cultural setting of Minnesota or Wisconsin. While cooperatives are great for certain kinds of businesses, they’re not for everyone: They can raise modest sums of capital, but struggle with large sums; their structures aren’t always flexible enough to accommodate multiple capital classes; their plodding, consensus-based nature makes them resistant to entrepreneurs’ bold ideas. Big-money equity investors (aka venture capital) are critically important to getting small businesses going, and are rewarded with high returns and an outsized say in governance — neither of which can be accomplished with a co-op’s flat structure.

The history of Minneapolis’ West Bank neighborhood is an instructive example of co-ops’ promise and limitations. Uniquely among the ’60s hippie havens, federal urban renewal was leveraged to place most of the neighborhood’s housing stock within limited equity co-ops or Section 8. Alas, idealism and local control proved unable to adapt to either obsolescence or succession [PDF]. Photo: Michael Hicks, via Flickr.

Which brought us to the big small-business finance innovation of recent years: crowdfunding. Numerous “community investing” vehicles have been floated, like direct/P2P lending, lending through community financial institutions, conventional Kickstarter-style rewards (perhaps with interest paid in-kind), equity investments, etc. Crowdfunding has become almost de rigeur in certain popular, high-growth businesses. It first swept thin markets for trinkets that would typically be distributed online — e.g., board games. As the dollar amounts have grown, and as regulators have gradually warmed to the idea, platforms specializing in more capital-intensive bricks and mortar projects have sprouted for sectors like breweries and restaurants. Business models that defy categorization, like the McMenamin’s brand of alcohol theme parks, might be particularly well-suited to crowdfunded equity.

Several new platforms have emerged within this space. I’m most familiar with Fundrise. It’s evolved its primary offering away from common equity investments and towards what it calls “project payment dependent notes,” a hybrid of mezzanine debt (it’s debt, with a promissory note) and preferred equity (even though there’s a pre-determined target return, dividends are only paid when there’s adequate cash flow). For small developers, crowdfunding — even in the currently half-baked, accredited-investors-only form — holds significant advantages, namely cheaper, slower money, plus broader community buy-in.

Interestingly for our purposes, at least one nonprofit community development institution has begun to use Fundrise as part of its capital stack, and in particular in an attempt to save a for-profit community institution. The San Francisco Community Land Trust used Fundrise to raise its 38% equity stake (a local nonprofit offered the other 62% as equity) in an attempt to buy a mixed-use building housing the nation’s oldest African American bookstore, in a neighborhood otherwise ravaged by urban renewal. (Alas, the attempt foundered when the landlord changed the offering price.) All that the city could do was to landmark the building, perhaps in an attempt to reduce its market value, and to offer the business inclusion on a “legacy business” roster.

Mezzanine debt seems to also be the sweet spot for small business-oriented lenders like ZipCap. Their business model mirrors the built-in customer base of a cooperative, “recruiting an ‘Inner Circle’ of customers who pledge to spend a set amount of money in a fixed period of time.” Instead of relying upon just that circle for funds [as a co-op would do with equity memberships, or Member Loans], ZipCap uses those pledges as collateral for outside loans.

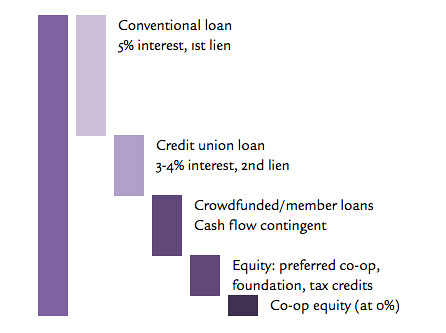

Combining all of the above vehicles — not-for-profits, low-profit cooperatives, and crowd funded for-profits — into interrelated entities might solve the scalability problem by allowing each entity to contribute its own strengths to a capital stack:

We called this entity a Place Corp, which has the ability to construct a capital stack from various tranches of capital, while keeping control within the community. (Outside investors and developers can help to build pieces, with the Place Corp hopefully maintaining some control via equity, but are treated merely as means towards an end.) Investors can choose from a wide variety of risk/return combinations, and can invest either time or money, choosing negative returns (gifts, grants), zero return (co-op equity), or modest returns. The Place Corp is diversified across property types, but not in location — like the family firms or community banks of yore. The durable, long-term returns of placemaking will create financial rewards for some investors — but for most, the place itself will be the return.

Next in the series: Where? And what sort of services might a Place Corp provide beyond just financing?

Thanks to some of those who contributed to this series of conversations: Karja Hansen, Matt Lambert, Russell Preston, George Proakis, Padriac Steinschneider, Seth Zeren

Payton, I am curious if all the additional governance and compliance of co-ops and place corp.s are needed. If people have the wherewithal to develop or redevelop a place have they decided that the more direct route of just being a developer of buildings held in portfolio is not workable? There is no shortage of small investor capital for decent real estate projects, but there is a shortage of people who can execute projects in an urban context.

You’re correct that it’s not “needed.” In most smaller cities, your diagnosis is correct: there’s a shortage of good people, and plenty of good opportunities with entitlements in place.

In other contexts, where neighborhood distrust of change is a primary barrier — and where entitlements are tough to get without that trust — a Place Corp could be a trusted vehicle for neighborhood change. It offers literal buy-in, as well as a promise of longevity and community control. Individual developers, unfortunately, usually have to work very hard to earn that sort of trust.

Pingback: Friday photo: Be careful what your zoning asks for | west north

Payton,

This is a great summary of some of our ideas leading to and coming from the Place-Corp idea. Beyond a new way of structuring the capital for smaller, incremental infill development projects, I think P-Corps could create a few other advantages:

1) A place between the private developer and the community that could receive community benefits packages (from developments) and implement them (where the City was unable/politically infeasible), such as operating/programming community spaces, lower cost commercial spaces, parks, etc. (a role sometimes filled by BID’s, CDC’s, neighborhood arts organizations, and others depending—but could be more strategically followed through by the P-Corp)

2) Venture capital for small developers: One of the problems that small developers who would do the small scale incremental development we say that we want have is raising seed capital to get the project going. We need a venture fund that is place/neighborhood focused that can spot the fire in the belly entrepreneur and support them with patient capital and training (as in VC), but with a longer time horizon/lower expected returns and the opportunity to benefit from positive externalities from the new development on existing P-Corp projects, rather than pure returns from the project (more in the credit union space).

3) Capability to do planning, programming, tactical infrastructure work: Similar to 1) above, the P-Corp would be able to engage in its own planning, programming, engagement, and tactical projects—pooling the overhead of many projects to do more comprehensive work, and able to carry freight for long term vision items such as street redesigns, etc. that a single developer is less likely to want to do. (Sort of like what a BID or City might do, but more connected to actually building the buildings that relate/benefit from it)

4) Master developer role vis value capture: along the lines of the above, the P-Corp might work more as a master developer, building some projects directly, permitting other parcels and selling them off to smaller operators, etc. This allows them to benefit from positive externalities and synergies between properties in a way that a too balkanized ownership cannot. It may also help coordinate leasing strategies to avoid Bank-Badlands and Nail Salon Ghettos.

5) Problem of complexity caused by combination of so many capital types: One friendly critique I’d offer of your post’s discussion of financing mechanisms is that the multi-tiered model that you offer may ultimately be as complex (and high in overhead) as the typical LIHTC CDC model, making it pretty far from Lean, and potentially hard to coordinate with smaller operators. I’d be interested in having an equity pool that contains a simple model for existing and potential residents/operators to participate in “owning” their place but combines it with placing large equity sources from outside that’s looking for better than 2% returns. And finish off with a hunk of debt. 5b) The challenge I see with too much local ownership is going to be the coop problem of increasingly cumbersome decision making as more people want the P-Corp to work toward their ideas…

Seth

Pingback: CNU conversations: Striking before the neighborhood’s hot | west north