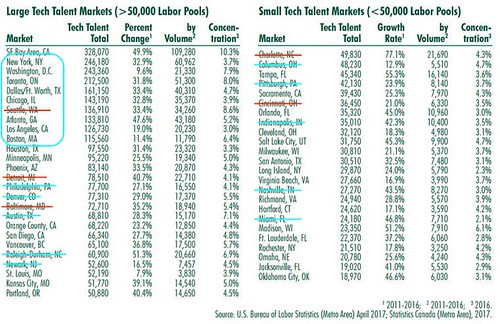

Last September, I pointed out that the Amazon HQ2 RFP was almost entirely about site readiness and talent. On the latter topic, one excellent resource was a 2017 report from commercial real estate broker CBRE that ranked metro areas based on “tech talent” — the number of people employed as “software developers and programmers; computer support, database and systems; technology and engineering related; and computer and information system managers.”

Not too surprisingly, eight of the top 10 from that particular ranking ended up as finalists for Amazon’s HQ2. The other two are Seattle (HQ1) and the Bay Area, which is currently Amazon’s second largest location.

Top 10 (minus SF) circled in blue; cities officially ruled out for talent reasons in red; shortlist cities with even smaller talent pools ruled out in blue. Source: BLS, via CBRE.

A single theme keeps showing up in the “thanks, but no thanks” feedback interviews. “Talent was the most important factor out of everything they looked at,” said Ed Loyd of Cincinnati. Charlotte’s “pool of tech talent is lacking compared to other markets.” “We weren’t good enough on the talent front,” said Sandy Baruah of Detroit. Amazon “really emphasized that they put a high weighting on talent,” says Mary Moran of Calgary. “Talent that could be hired immediately… ‘it was clear from the earliest stage of the RFP that it was the top priority,” says Tom Geddes of Baltimore. The feedback got more specific in one instance: “Prince George’s county doesn’t have a large enough pool of senior-level software engineers.”

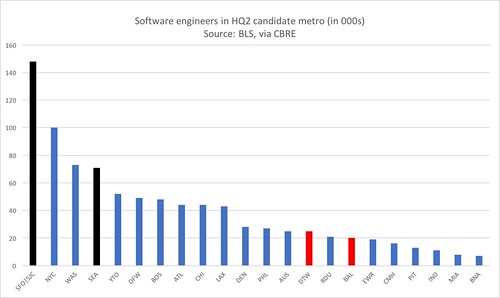

Now that we know that Detroit and Baltimore don’t have enough local software engineers, who does? Helpfully, CBRE also looked specifically at the software engineer labor pool.

HQ2 candidates are in blue, Seattle and the Bay Area are in black, Detroit and Baltimore are shown in red. Click to enlarge.

There’s a substantial gulf between the top 10 and the latter 10, with Los Angeles having about 50% more local programmers than Denver. More importantly, if Detroit was rejected because they don’t have enough programmers, how can Philadelphia or Raleigh say otherwise? This puts the smaller labor markets on the shortlist at a steep disadvantage. Only Newark can make a case that it could pull commuters across the Hudson (though not for long).

Shallow talent pools also explain why “turnaround” sentiment wasn’t enough to save bids from Rust Belt cities. The only Midwestern cities that made the cut are either Sunbelt-era cities that happen to be north of the Ohio, like Columbus and Indianapolis, or the classic turnaround success stories of Chicago and Pittsburgh (even if both have deeper post-industrial legacies than the coastal cities).

A bit less confidently, recent large office leases in Boston and Manhattan are probably best thought of as consolation prizes, given that the locations chosen don’t have much in the way of expansion options. Leases being negotiated now would reflect planning work that was underway before the HQ2 search got going. [Update, 1 May: not alone on this reasoning.] Recent warehouse and data center leases or openings, of course, have zero bearing on future office locations.

The Boston move also has implications for cities 5-10 in the above chart, all of which have ~45,000 programmers. Quality of local talent is also important, and proximity to MIT gives Boston an edge over others in this group. If Boston and NYC are only worthy of consolation prizes, who’s left?

Hint: it’s also the metro where not just the number of programmers most closely matches that of Seattle’s, but their skill sets do, too.

Other thoughts:

- Reporters are so desperate to write anything about this story that they’re making mountains out of molehills, especially given the paucity of public information. Don’t read too much into:

- Paddy Power betting odds, which explicitly exclude the Americans who might know anything about the cities. I don’t see British newspapers breathlessly tracking every movement in how Vegas bookies view the English Premier League.

- Hiring a lobbyist in Georgia. They have lobbyists in other states (e.g., two listed in Virginia, five in Kentucky, three in Tennessee).

- Amazon really does seem to prefer working with single developers. Just one developer (COPT) has a four million square foot portfolio of Amazon data centers in NoVA.

- The already-tight timing is now getting a little ridiculous. The decision will be announced sometime in 2018, presumably not in the next few months — but occupancy is still supposed to be in 2019? That essentially limits the search to existing buildings.

- Given that fact, I’m going to give a Top Three that combine the right site, the right workforce, and the right time:

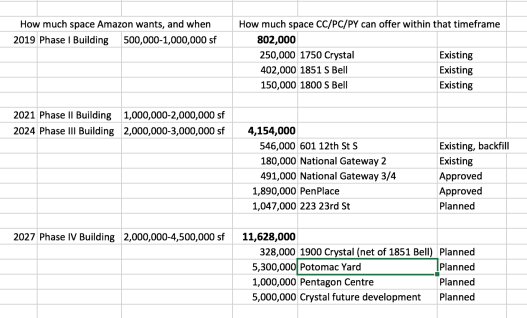

- Arlington – Crystal City, the only move-in-ready location with access to as many programmers as Seattle has

- Update, 25 Apr 2018: Others share this prediction

- Update, 15 Sep 2018: Someone suddenly seems interested in Crystal City offices. As recently as January, JBGS filed plans to switch 670,000 sq ft of office capacity to 665 apartments. As recently as August, the CEO’s quarterly letter to shareholders promised a company-wide pivot from office to residential. Yet… In July, they retracted 1750 Crystal’s conversion, puzzlingly adding back 250,000 sq ft of office to a block with 551,000 sq ft empty. The result fits in neatly with a short, medium, and long-term occupancy strategy for HQ2.

- Chicago – Old Post Office, the perfect building with great access and aggressive leadership but more iffy growth potential

- Dallas – Union Station, although the buildings require considerable work. (Not that Amazon’s RFP mentions this topic, but: right-wingers love to harp on Chicago’s fiscal woes even though Dallas isn’t far behind.)

- Arlington – Crystal City, the only move-in-ready location with access to as many programmers as Seattle has

- Expanding to a Top Five adds: